Why You Should Offer These Core Financial Planning Services

July 13, 2022

When we saw the results of the 2021 Cerulli Associates survey of RIAs, we were not surprised that more than 80% of those surveyed offered retirement income planning and retirement accumulation planning. On the other hand, far fewer RIAs were offering services that we consider part of core planning—including tax planning, educational funding, estate planning, and insurance needs analysis.

This survey helped inspire our June 2022 Finlocity presentation, “How to Make Financial Planning a Breeze for You and Your Clients”. Ted Denbow, VP/Head of Sales, walked through a case study showing how advisors can address these important services easily within RightCapital’s financial planning software, services that 4/10 RIAs are not offering.

...how to make financial planning a breeze for you and your clients. For this session, we're joined by Ted Denbow. Ted, I knew I was going to mix that up — I was thinking Tim Tebow in my head. Ted is the vice president and head of sales for RightCapital. Ted, we're going to pass over the controls. It's all yours.

Excellent. Thank you very much, and thank you everybody. Very happy to be here. We're going to take the next little bit of time and show you how RightCapital helps make financial planning a breeze. So let's move right along into the content here today.

Just a quick background on myself. I've been in the business for over a couple decades — every time I say that it makes me feel older. I've been working with advisors for quite a while in many different capacities, even as a registered rep for a period of time. RightCapital started in 2015. I started right away, essentially within eight months of them launching. I was on board, and we were still working in our CEO's garage at that time. We've come a significant way. We started just under seven years ago with the sole focus to create the best planning experience we could for advisors.

How we became the fastest growing planning solution on the market and top rated has a lot to do with our approach. We want to give a solution to you, the advisor, that allows you to engage your clients the way you see fit, and gives you a platform that has vast capabilities but is easy to use. That is a challenging target, and we've done that quite well. You may have seen the Michael Kitces surveys and the T3 surveys — not only are we well established as a third of the market against Goliaths like eMoney and MoneyGuide, but we've also had the highest user satisfaction ratings. That comes back to our approach, giving you a solution that allows you to support a broad array of clients and interact with them in the best way possible, but also a modular platform that allows you to evolve and iterate in your planning process. So you can focus on what's important to them, but also interact with them and modify your approach as the plan changes, as things change like the environment we're in these days — with high inflation and crazy volatility in the markets, being able to have a flexible platform can be quite helpful to show the different interactions and approaches.

So let's jump right along. We look at planning as a whole — it means different things to different people. We looked at a lot of different research surveys and studies, and saw one that really hit on one of the aspects that helps you do more in planning with RightCapital. When you look at what people do in planning, of course most all advisors focus on retirement planning, accumulation for retirement, and so on. That's at the core of what everybody does. But surprisingly, some other areas we'd think would be fairly core to their offerings are only done by about 50 to 60 percent of advisors out there — things like college planning, insurance. Insurance is a big area of opportunity and big value to provide clients, assessing the needs. Whether you're able to sell or position life insurance or not, at least evaluating their approach can be quite beneficial to you and to the clients. Budgeting and cash management is a key part of it. Another one we all talk about a lot but isn't always baked into the overall plans, and certainly not into every planning solution out there, is tax planning — and actually detailed tax planning. The last one depends a lot on the client types, their net worth, and so on, but I think we'd all agree there's definitely some aspects that affect a good amount of your client base when it comes to estate planning. And certainly when you think about potential policy changes that may be coming down the road, it may affect even more of your client base than it currently does.

So while those are pretty complex scenarios, how can you make that easy? How can you make that part of your regular planning experience? That's what we're here to do at RightCapital — try to help make it easier to implement these different areas. If you're not doing them already, or if you're doing them already, we think we can help you make it a little easier even in the process you're doing today, to be more interactive around tax planning, education planning, insurance, and estate planning. And finally, one of our new areas helps wrap all this together: making it easy to have recurring updates with our new one page plan, which we'll spend a little time on. And at the end we'll have time for questions.

So let's dive into some of the content here. We're using a baseline case study today. These are the folks we use in some of the examples. Let's meet the Bradys. I'd guess these are probably similar to a lot of your clients in your client database. They're in their late 40s, with a couple of tweens. They're going to live well into their 90s in most cases. They're looking to retire a little bit earlier — who wouldn't like to retire at 60? Decent earners, about $250k a year, average expenses of $10k a month, and some reasonable assets — over $400,000 in both qualified and non-qualified, money set aside for college in some 529s, and a little bit of cash. I'd bet that's fairly common to at least a reasonable percentage of the clients you work with.

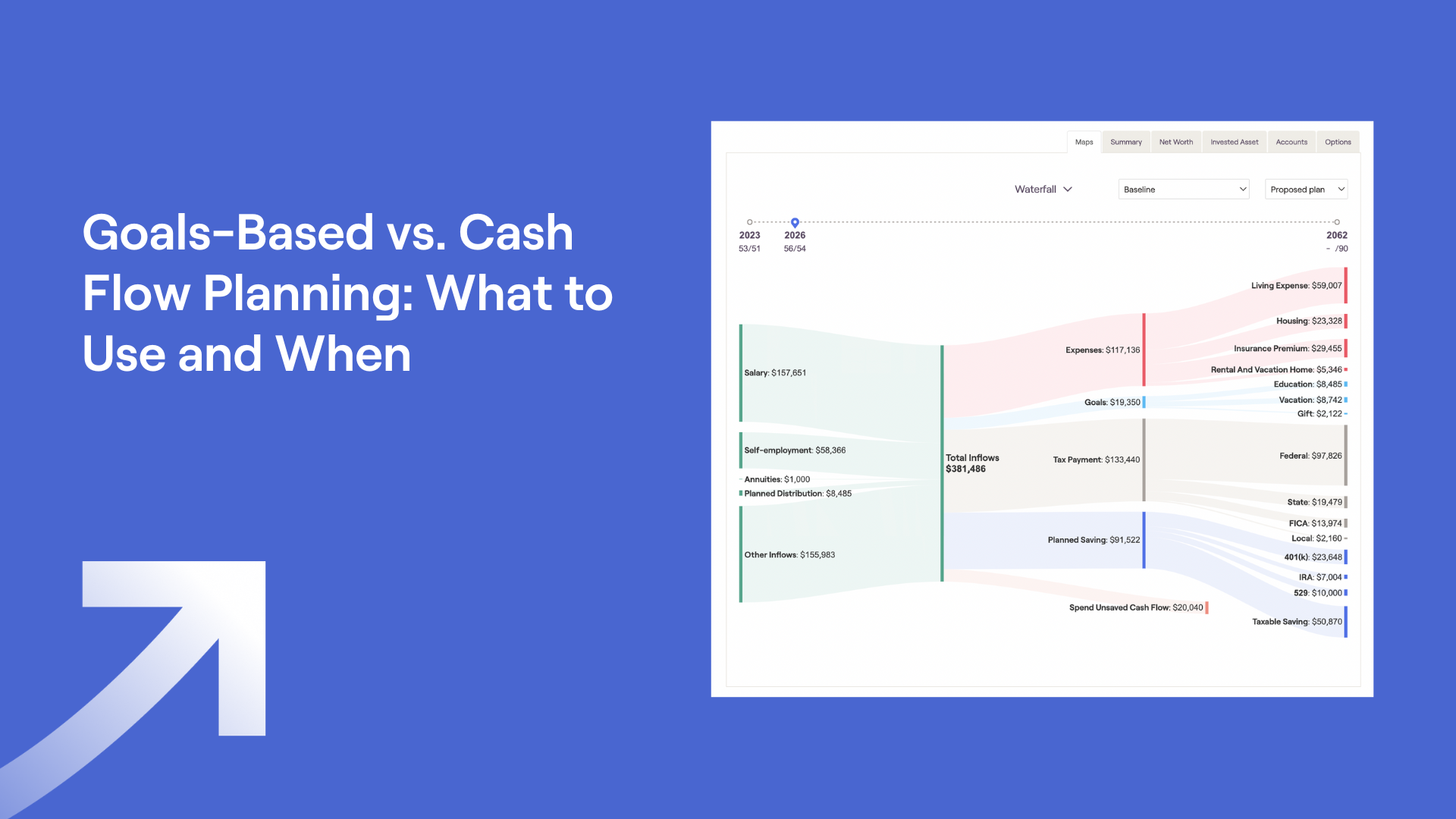

So we look at them across those areas we talked about. One of the biggest things we've seen time and time again, and this is really at the core of our offering, is interaction — making it easy to work interactively, to modify things on the fly. Whether that's in person with the client — and I know more and more folks are back to normal office meetings — or through virtual interactions, whether it be Zoom or GoToMeeting or whatever it might be, having a platform that allows you to easily adjust and adapt is at the core of what we offer. One of the central points of our planning solution is our analysis area. It's really the assets and planning tool that brings together all the elements of our platform, looking at the overall probability of success. The current plan is their baseline, and proposed plans are what you're recommending or suggesting as possible changes. On the same screen where it presents that is where you actually build and modify the plan, right there. You don't have to leave that window, go somewhere else, make a change, generate a report to see what happened. You change it right here on the spot by adjusting the slide bars or modifying some of the inputs — anything across their goals, expenses, saving strategies, investments, Social Security, or even insurance and other needs. You can follow those in and it'll let you modify them and show the effect. We have many advisors that will build some or even all of that recommendation plan on the fly, because it allows you to make a change, show the effect of the change, and many advisors like that because it helps them more easily explain why they're making that recommendation. So this is at the core of our platform.

Let me dig into some of the other modules. You have additional views that let you see not just the probability of success, but the comparisons — how much more they might be saving across that particular recommendation, whether it's total net worth, total assets, even taxes, how much more tax advantaged one plan versus the other might be.

Speaking of that specifically, let's talk about tax planning. This is one of our more unique areas — a true tax planning component built into our platform. You can use this or not; everything's flexible and modular. You can decide what elements you feel are relevant to that client. This lets you look at a multitude of items. We actually project and populate federal, state, and FICA taxes — we calculate that for you. It's not just using average brackets; it's basing all these projections on the actual AGI numbers inside the platform, so we can show you when they're going to hit those brackets. When we look at things like retirement, we all know that if they've done a really good job accumulating that wealth, and maybe a lot of it is in tax deferred assets, what's going to happen when RMDs kick in. They may be looking at rather large RMDs because there's so much money in there, which means they may be bumping up quite a few tax brackets, especially when you layer in Social Security, pensions, and other distributions. So it could create a big tax issue.

We make it easy to look at two things here. One, you can quickly look at the timing of the distributions across the tax brackets — is there a more efficient way to draw down those assets? And then, when they're in a lower bracket, is it worth looking at Roth conversions? You can simply slide the bar over and set the bracket you want to fill up to with Roth conversions whenever they're below it, and we'll calculate how much they can convert without exceeding that bracket, and see what that value might be. In this case it could be over two million dollars in savings by applying a different timing of the distributions and looking at Roth conversions. So that could be quite impactful.

We go a little further, looking at federal, state, and FICA taxes. In this case, we can see they might be in a lower bracket in their mid to late 60s, which is the area where Roth conversions might make sense. We can look at a multitude of different views. We even go so far as to project and populate their 1040 and most of the sub-schedules over all years of the plan. So if they're looking at maybe liquidating a bunch of stock options, that could be quite impactful depending on where they are — it might bump them up a bracket, maybe put them into the joyous event of hitting AMT for the first time. You can model that out and show them what that could look like based on the scenario you're highlighting. And if you have a different approach you might want to recommend, you could show them the difference that would make, not just on their plan, but on their actual taxable event that may occur. So it's quite powerful. People really enjoy and find a lot of value out of this ability to do these very complex projections and put it in a visual that people are generally familiar with.

We go on to college planning, which most people talk about in some capacity with their clients. But are you baking it into their overall plan? Within our platform we link up to all the different university databases. So if you already know where the kids or grandkids are going, you can select it and it'll pull in the tuition cost. We even break it down — in-state versus out-of-state for state schools. It'll let you look at where the money's coming from. Maybe they've got 529s like they do in this plan. Is there any additional opportunity for student loans or scholarships? Do we want to fund it just out of 529s or other assets? How much more do they need to save to fill that gap? Not everybody wants to pay 100% for the kids — some people like to have the kids have a little skin in the game, so you can calculate it out. Maybe they want to cover 90%, so you can determine how much is left over that the kids will be responsible for. Our tool lets you easily adjust those on the fly and very interactively with the end client.

Then we look at another complicated area with a lot of moving parts: insurance needs. And not just life insurance — we look at a multitude of areas. We have a few different life insurance tools. We also have disability insurance assessment, LTC, even P&C. On the insurance side, the nice simple calculator we call our human life value calculator is looking at just the replacement income. This is often where folks will start. Maybe it's a new married couple, they have kids, and they want to look at 10 or 20 years. You can look at it: if we just want to replace their income, here's the insurance they need to cover the gap between now and retirement. You can even modify tax brackets and discount rates, or reduce the number of years it's targeting. This is a quick and easy way to look at that right in our platform.

From there we take it a step further and look deeper into those insurance needs, looking at the protection need if one of them dies, to keep the whole plan intact — to keep the surviving spouse and kids and grandkids hitting all their goals, covering all their expenses and needs, managing that cash flow and keeping everything sustained. You can quickly assess that and then dial it up or down from there. Maybe they're just looking to cover the mortgage and college. Because our platform is easily interacted with on the same screen, you could go in and modify any of those elements of the plan and it'll recalculate that number. What's really nice is it goes even further and does a full cash flow projection, so you can see, without that insurance, when they would run out of money. That can be quite impactful when explaining why the insurance might be a worthy discussion.

Let's jump more into the estate planning side. This can get complicated. Not everybody has detailed estate needs, and there's a lot of arguments on both sides, but everybody should at least look at who their beneficiaries are. It's something that's easily overlooked. So we have a nice simple one-page view where you can map out all their beneficiaries to all their different accounts and policies. I used to travel with this a lot back in the day, and I used to hear those horrible stories where, unfortunately, one of the spouses passed and they hadn't updated their beneficiaries, and everything got paid out to the ex prior to that scenario. So we all can appreciate not wanting that to happen to any of our clients, and often it's just something that gets overlooked. A nice simple review of this can make it easily visible to the clients. And one thing I didn't mention already is we have a full client portal, so you can give clients access to any or all of their plan. We make it easy for you to not just build and interact with the client, but actually give them access to all this information so they can review it. What's nice about our solution is you can send them a reminder — maybe just do an annual review of their beneficiaries, even if it's outside of your normal interactions. The system will tell them, take a look at your beneficiaries page, see if anything needs updating. A simple thing, but it can be quite an important task — if overlooked, it can create some challenges.

On the other side, we get into more complex and detailed estate planning. We have a nice simple flow chart that highlights what's in the estate, what's out of the estate, and how those assets would pass on to the spouse and to the heirs. That can be helpful even if they're not a high net worth or ultra high net worth person worried about the exemption limits — still being able to show what that could look like, because we calculate it for all the federal tax scenarios. From there, you can layer in a multitude of trust strategies. So if you're dealing with higher ultra net worth clients with more complicated estates, and you want to model more complex trust strategies, we have all those capabilities. Not only can you build them in if they're already in place, you can propose one or multiple different strategies and see what effect it would have — everything from credit shelter trusts to CRTs, ILITs, GRATs, SLATs, and grants. If it's applicable to them, you can model it quickly and easily in the platform and show the effect it would have on taxes, the heirs, charities, and their income, if it's going to have an impact on their income over that span. You have the ability to really drill down and expose what that could look like. One or multiple — so you can show, if you have this trust strategy already in place, here's what it looks like if we layer in a CRT, or an ILIT.

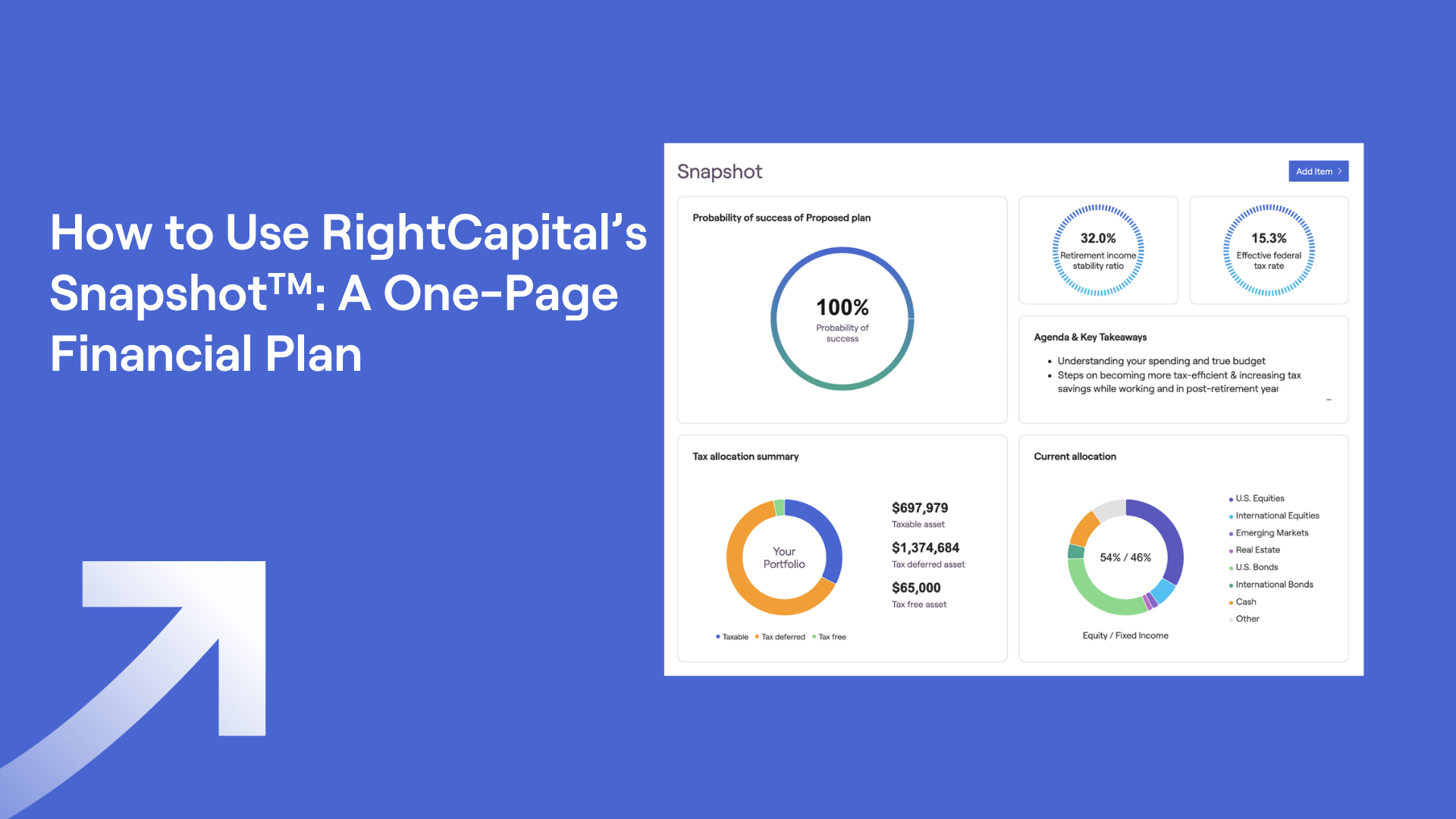

One final highlight of our platform is what we call our Snapshot, more often referred to as the one-page plan. This is something many advisors build on their own regardless of what planning tool they have — they take little bits and pieces, different charts, and create their own output. That's time consuming and difficult, and we wanted to make a solution that helps you achieve the same results but makes it really easy to use. This is what it looks like. It lets you pull in many of the different charts, elements, and widgets within our planning tools — all fed by our core plan — and create a one-page view of things that are important and relevant to that client: their proposed probability of success, their current net worth, savings rates, tax rates, their Monte Carlo simulation. You can pick and choose the different elements you want to have in there to build a one-page view that's most applicable to that client, and then you get to reorder them — you can move all those images around by clicking, dragging, and dropping. So you could put what's most important at the top, and layer in any other items.

Since we rolled this out, most of our advisors really use this for follow-up meetings with clients, but you can certainly use it for your initial review. It's not only a printable output — you can print a very detailed full plan with 20, 30, 40, 50 pages of detail and cash flows — but if you want a nice simple one-page view, you can not only print it, you can make it their dashboard. So that's the first thing they see when they log into their platform. Think about the value that can bring to an end client, particularly at times like now when there's lots of volatility, impacts of inflation, and other things occurring. Most clients want to know not just whether their accounts are up or down, but am I going to be okay, am I on track? Having the things that are most important on that first screen they see when they log in can really help drive that home and ease some of that emotional vulnerability we all have when markets are a little haywire like they are today. So that's been incredibly popular for us. It's something new we just rolled out, and it even lets you add in text boxes and details, so if there are things you want to call out and spend time talking through, you can easily do that. And you can modify it anytime, both for their digital view and their printed report.

Let me go into one other quick area, and then we'll get to the final few minutes with questions. Let me talk a little bit about some of the additional things we offer. I highlighted a lot in there — we do all the core things you'd expect with retirement analysis and retirement planning, but layering in those other elements: insurance needs, education planning, tax planning, estate planning. We also do other things to support other types of clients. We have a budgeting and debt management tool. We have the only student loan module available in a full-blown planning solution. So we support a broader demographic of clients, not just your pre-retirees and retirees. We also have more insurance capabilities beyond just the standard life that I highlighted, and some debt analysis that lets you look at different pay down strategies. We have aggregation, where clients can link up their outside accounts, and you can involve them right from the beginning. We have a full digital onboarding platform that allows clients to enter as little or as much data as you want.

We'd love to show you how this works. We offer full demo access, so you can set up a call to review everything on how our platform works. We also give you the ability to test it — it's important to take things for a test drive to see how easy it is. A lot of our success is really driven by that ease of use, but we do it in a manner that doesn't limit the planning capabilities. Our goal is to give you the ability to make financial planning a breeze, but also to do more planning — to work with more clients and more types of clients. Even if they're not your target market, some of those capabilities can help you strengthen or broaden your relationship with your existing client base. To use one quick example, think about student loans. We have a student loan module that looks at their potential eligibility for some of the federal programs, how it might save them money, even cut off some of the balance. Folks with student loan debt may not be your target market, but odds are their kids, grandkids, nieces, and nephews probably have some student loan debt. So when that conversation comes up, you have a module you can send by itself out to the extended family member to look at what might be available to them. So hopefully that rounds out the picture: a platform that lets you drive the clients where you think is most important and relevant to them, giving you a really interactive and highly engaging platform, because both you and the clients can interact. You have the ability to give the clients the opportunity to interact with the tool. If you want to let them play around with the slide bars or adjustments, you can do that, and in a manner where it won't break the plan — we even have a setting where you can let clients make a change but it doesn't save anything, so when they log out and log back in, it goes back to what you originally put in front of them.

So hopefully all that comes together to show you why we've been very successful in helping advisors help more clients in just a short period of time, and why we at least think we're the best platform out there. The third parties and surveys tend to show we have some pretty great satisfaction ratings, not just there but also in our customer service and support. We'd love the opportunity to walk you through and show you why we think we can help you do more. So I think we're right at the top of the time here and ready for questions. I'll turn it back over to Chris.

Ted, great presentation, by the way. I love your energy. You're obviously very good at presentations — I think every company should hire you to do that. Okay, so we do have a question coming in, and they're asking: how much does RightCapital cost?

Great question. Of course, what's it going to cost me to get on board? A unique thing is that we're live today. We have different tiers of subscriptions. It's all advisor based, per month, or you pay upfront for the year. It's going to be $149.95 per month for basic — our core planning tools. We have our premium, which most everybody uses and is what I highlighted mostly; it includes our aggregation and other features, at $209.95 a month. And then we have platinum, which is more like enterprise for larger teams, at $254.95. (Most current pricing as of Summer 2026.) That's the price that starts tomorrow. I know it's last minute, but anybody who wants to take a look today can give us a call, jump on our site, and look at the platform. If that happens to work out, you could save anywhere from 20 to 50 bucks a month. Relative to the market, even with the prices going into effect tomorrow, we're still one of the more reasonably priced cash flow planning solutions out there.

Very cool. Okay, second question: is your planning software cash flow based or goal based?

So, as I noted, everything I highlighted here was one of our cash flow approaches, but we actually do both. You have the ability to do cash flow or goals based, and you can switch it anytime. That gives you flexibility. Some advisors might be starting out with a real basic conversation and just want to look at a simple goals-based approach, then as that evolves, you can convert it to a cash flow based plan and do a more detailed plan.

Very cool. Someone's asking, how hard is it to move plans from another financial planning software into RightCapital?

That's a big question we get. If you've been out there using whatever platform, you may have a lot of data in there, and migrating it is usually the big challenge. The answer is, it depends. We have a lot of integrations with all the different custodians, reporting tools, and CRMs. So any data that sits in there is easily pushed over. The data you have to manually convert — which is the same with any planning tool — is your goals and your income and expense data. With our solution it's easy to enter information, so it's usually not too bad. We usually recommend, if you have a hundred plans, you allow a 30-day overlap to migrate those plans — not because it's going to take you 30 days to recreate them, but to give your clients time to log into the new portal, update their accounts, make sure they know their password, simple things like that. We also have relationships with paraplanning firms that, for a fee, will do it for you.

Okay, one more question. Can I replace my tax planning software with RightCapital?

The answer is most likely. We've seen a lot of scenarios where folks might have different tools out there, like BNA, to do some projections and analysis. We've seen advisors that might have a Social Security optimizer tool and another planning tool, and we've seen many scenarios where they've dropped all three of those, and RightCapital supports their needs. Certainly, if you're doing current year tax plans, that's not what we're doing — we're doing projections and analysis. But if you're looking at something like a BNA, we've seen many folks drop that, if they just need the components we have, because our taxation is pretty powerful. You can really drill down and do some detailed projections and scenario analysis.

Okay, we're good on time, but did you have anything else you want to add? We have about a minute left.

Yeah, no problem. Like I said, we'd love the opportunity to show you what we can do. At a minimum, we see advisors save anywhere from 30 to 40% of their time spent on planning when they switch over to us. Like anything, there's a learning curve, but even that is pretty quick. I've seen advisors get up and running and presenting plans in a couple of days, but on the long side, maybe it takes two or three weeks. We give you an onboarding specialist who is your key point of contact for your first two months to make sure you get everything running, help you with your first couple of plans, and make it a breeze. That's our goal — simplify the process but not limit your capabilities.

Time is money, Ted. We'll let you get your time back and let you go. Thank you so much. We appreciate it. Great presentation.

Thank you. Really appreciate it.